SHADES OF CLOUD

The best product which does not wither over time, usage and ruggedness – The Mind. With such a product at hand, there is no upper bound but infinity to innovate. People had put in mind to improve rocket science, fluid mechanics, pharmaceuticals, genetics, carpentry, food production etc. A common unique thread which spans into all of the defined industries – Information Technology. When people started to apply mind to it, it was an incredible success.There were a lot of advancements in the software space and everything was targeted at how to build the software and perfect it. Decades of effort were spent on decoupling software from hardware. With perfection in creation of software, mind has hopped on to the “Run of software”. The game has just begun, the investment in this space is huge…

As a typical CIO or a Chief Architect, one would have the IT budget of 33% on App Development & Maintenance and 67% on the Infrastructure & Cloud run. While the Application development and maintenance has considerably matured over the past few decades, there is a potential to innovate and optimize on the 67% spend! A careful adoption of Cloud could result in addressing this.

To derive value for money, let us look at the three shades of cloud which contribute to the major part of a CIO’s spend,

- 1. The SaaS – True Digital Story

- 2. The IaaS Play – The three giants

- 3. Software Defined Converged Infrastructure story to unlock the on-prem potential

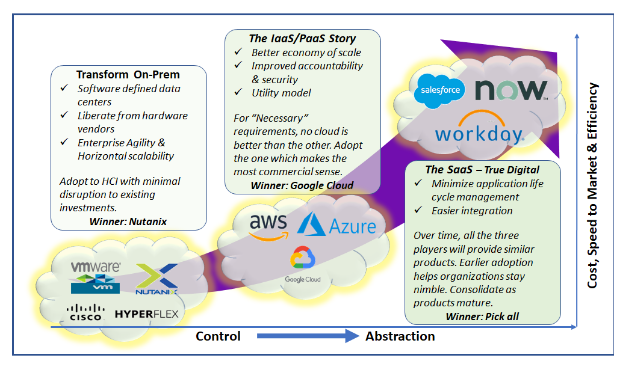

The SaaS – True Digital storyBack in early 2000s, I was all excited to create products to manage compute, create “Line of sight” for storage usage, backup efficiency etc. They were used to optimize the utilization of IT assets. It took a 3-digit person hours for me to build each product for the bank I was employed with and it was equally complex to maintain by my team.

Almost two decades later, when I think about it today, no one is interested in spending time and money on such boiler plate products. Pick them off the shelf or off the cloud. We should discuss about “The Cloud Born” companies – SalesForce, ServiceNow and Workday. These 3 SaaS companies came in to drive the Digital Transformation for Corporate Applications – ~30% of any CIOs budget. They enabled the transformation not just for the large enterprises, but for medium sized organization as well. They started to address three different areas in the Corporate Applications Infrastructure. One chose CRM, the other chose ITSM and the third on Human Capital Management. They perfected the offering in their respective areas. For example, with 20% global market share for CRM , today SalesForce is 2X of SAP and 3X of Oracle (Ref 1).

The interesting phenomenon happening here is, each one of them started getting into other areas. A large part of ServiceNow ITSM functionality can be achieved using SalesForce. Workday can do a good part of financial management done by SalesForce. All these players continue to innovate, and they appear on the Forbes top 3 innovative companies in the world (Ref 2).

The more I work on these platforms, the more I am convinced, they are not going to be monopoly on their respective areas – but will offer similar solutions in the longer run and compete.

As a CIO, one should minimize the home grown and go with one or more of these three depending on the current needs. Sooner, you would be able to switch between these three, avoiding the risk of vendor locking. As a buyer I can’t take my eyes off the perfection and quality offered by these Digital Disruptors!

The Public Cloud Story

The three cloud giants AWS, Azure and GCP try to differentiate the offerings and show them as ideal for different use cases. With all due credibility AWS is the pioneer in the public cloud sales and within these three, we can approximate 69% of the market share for AWS. Azure to follow next with about 23% and GCP at 8%. I approximated this with $45B, $15B, $5B for the three in terms of revenue.Why is Azure 3 times of Google Cloud and why is Amazon 3 times of Azure? I see four primary reasons,

Early mover advantage: Popularity is undoubtedly one of the key reasons for AWS leadership. It coupled with ease of implementing and managing AWS environment. It has enabled more “On the ground” ambassadors – the system administrator communities.

Loyalty: Most enterprises use Microsoft ecosystem on their datacenters. Because Azure is tightly integrated with those applications, the enterprises often finds that it makes more sense to adopt Azure. To top it, Microsoft makes the deal sweeter by offering license cost advantage.

Notional advantage of features: While decision makers are excited about the sheer number of offerings from AWS, the ever-growing portfolio makes it complicated to select the right product for the business needs. For example, Amazon RDS and Amazon Aurora provides a similar service on managed MySql. Though there are differences, it is difficult for an Enterprise Architect to understand the 150+ products and decide without ambiguity.

Cloud Economy: With greater innovation and stability by all the three vendors, this should play a major role in deciding the landing zone. My analysis shows, today with the discounting model, Google Cloud is comparatively cost efficient followed by Azure if the workload is predominantly Microsoft.

With that said, sooner there will be a baseline defined for the offerings which would cater to the nature of requirements,

- 1. Necessary requirements

- 2. Good-To-Have requirements

- 3. Surplus to requirements

As a CIO, if one pushes the architects to classify the business requirements into those three offerings, a better clarity would emerge. In most cases, one would land in Google Cloud as the economies work out today!

Though AWS takes the prize today on market share leadership today, the three vendors will hit the equilibrium in near future.

Software Defined Converged Infrastructure

As SaaS and IaaS would be the first two choices for the CIOs, the need for having OnPrem is never going to go away. We have the three major players here – VMWare, Nutanix and Cisco. According to IDC they enjoy the market share of 38%, 29% and 6% respectively leaving only 27% to the rest of the players including HP’s Simplivity3.

This is an industry which is going to completely change the way we build on premise Infrastructure. The need for expensive hardware is going away with white labeled commodity hardware (like SuperMicro). Software will define the datacenters, not the hardware. The new guy in this mix – Nutanix – is going to be more powerful than the other two. While all the three players offer great products, Nutanix has no conflict of interest. Dell/EMC’s storage business will try not to grow HCI software since it will impact their VxRail sale. If Software Defined Network is the norm, the need for Cisco expensive gears would reduce. Nutanix entered in this space as the hardware agnostics solution provider, and that will remain it’s core strength to innovate.

With that said, the most interesting part is the growth rate of these three players in the recent quarters (Ref 3). Dell/VMware grew at 40% when Nutanix grew at 5%. While Nutanix will continue to innovate, I expect giants like Google will attempt acquiring Nutanix and make it a strategic fit for private cloud. Even worse, Dell may try doing the same thing HP did to SimpliVity.

As a CIO, one should adopt Software Defined Converged Infrastructure and Nutanix will make a difference in this segment in the near run

To Conclude:

Lions are born knowing they are predators. Antelopes understand they are the prey. Humans are one of the few creatures on Earth given the choice. – Patrick H.T. Doyle

As a CIO or a Chief Architect, careful choice of SaaS, Public cloud IaaS and the software defined Converged Infra will play a major role in controlling cost and improve cost efficiency. It is not the sales pitch by these vendors, but the team’s ability to classify the requirements into “Necessary, Good to have and Surplus to requirements” will decides the success. While the CIOs help improve the IT, they also play a major role in creating a healthy eco-system in marketplace.

When you make a choice, you change the future!

Bibliography

https://www.forbes.com/sites/louiscolumbus/2019/06/22/salesforce-now-has-over-19-of-the-crm-market/

https://www.forbes.com/innovative-companies/

https://blocksandfiles.com/2019/09/25/idci-hci-market-leaders-q2-2019/

About the Author: Venkat Janarthanan – iamvenket@gmail.com

Venkat is a Director with a Global System Integrator specialized on Cloud Transformation for 13 Fortune 100 customers. With close to two decades of Infrastructure design and commercial modeling expertise, he has developed products on Public Cloud comparison and Operations Optimization on platforms including ServiceNow and Turbonomic. As a global citizen, Venkat has helped customers across the globe on modernizing their IT, bringing in transparency and improve efficiency. With Masters in Computer Science from IIT Madras, his passion is to create commercial models for IT Infrastructure and provide thought provoking insights to best utilize their IT investments.